< Engagement Rings / Engagement Ring Insurance

The content of this page is presented by Jewelers Mutual ®

An engagement ring is a valuable asset. Insuring it protects against loss, theft, or damage. There are several types of coverage—homeowners, renters, or standalone policies—but specialty jewelry insurance offers the most comprehensive protection. It typically costs 1–2% of the ring’s value per year to insure.

Protect Your Ring with Confidence

Jewelers Mutual Engagement Ring Insurance backed by 12,000+ 5-Star Reviews on TrustPilot

Your engagement ring is one of the most meaningful purchases you’ll ever make—a cherished symbol of love and a valuable investment. Given its high value and sentimental importance, insuring your engagement ring is one of the best ways to protect it against life’s unexpected moments, from accidental damage to loss or theft.

The right insurance policy ensures that if something happens, your natural diamond ring can be repaired or replaced without added stress. But not all policies are created equal, and understanding coverage details—plus any exclusions—can make all the difference. While homeowners and renters policies may offer limited protection, specialty providers like Jewelers Mutual offer coverage designed specifically for engagement rings.

✓ Covers loss, theft, and damage

✓ Protects against disappearance

✓ Works directly with your jeweler

If you’re wondering whether engagement ring insurance is really necessary, the short answer is yes. Your engagement ring is one of the most sentimental and valuable items you’ll own, and while no one expects the worst to happen, accidents, loss, and theft are always possibilities.

Unlike other types of jewelry, an engagement ring is worn daily, making it more susceptible to damage or being misplaced. Whether it’s a diamond coming loose from its setting, a ring slipping off while swimming, or an unexpected theft, having ring insurance ensures you won’t have to face the financial burden of replacing or repairing your ring on your own.

If your ring holds sentimental value—perhaps it’s an heirloom or custom-designed piece—having insurance that allows for repair or replacement with a comparable item is especially important. The right policy can help ease the stress of losing something so meaningful while ensuring you’re financially protected.

Policies from providers like Jewelers Mutual are designed specifically for everyday wear, offering protection where traditional insurance often falls short.

A comprehensive ring insurance policy is designed to protect your engagement ring against life’s unexpected mishaps. While coverage can vary by provider, most specialty jewelry insurance policies include protection against:

Loss

If your ring is lost, whether it slips off while swimming or disappears, insurance can cover the replacement cost.

Theft

If your ring is stolen, whether from your home, a hotel room, or even your purse, a policy can help reduce the financial impact.

Accidental damage

Engagement rings are meant to be worn daily, which means damage can happen. Many policies cover chipped stones, bent prongs, or broken settings, ensuring repairs are covered.

Disappearance

If you can’t pinpoint exactly when or where your ring went missing, some policies still offer coverage for a replacement.

That said, not all policies cover everything, so it’s important to read the fine print. Some exclusions may include wear and tear, intentional damage, or loss due to negligence. Always check with your provider to fully understand what’s included in your coverage, so you can wear your ring worry-free.

With Jewelers Mutual, policies typically include:

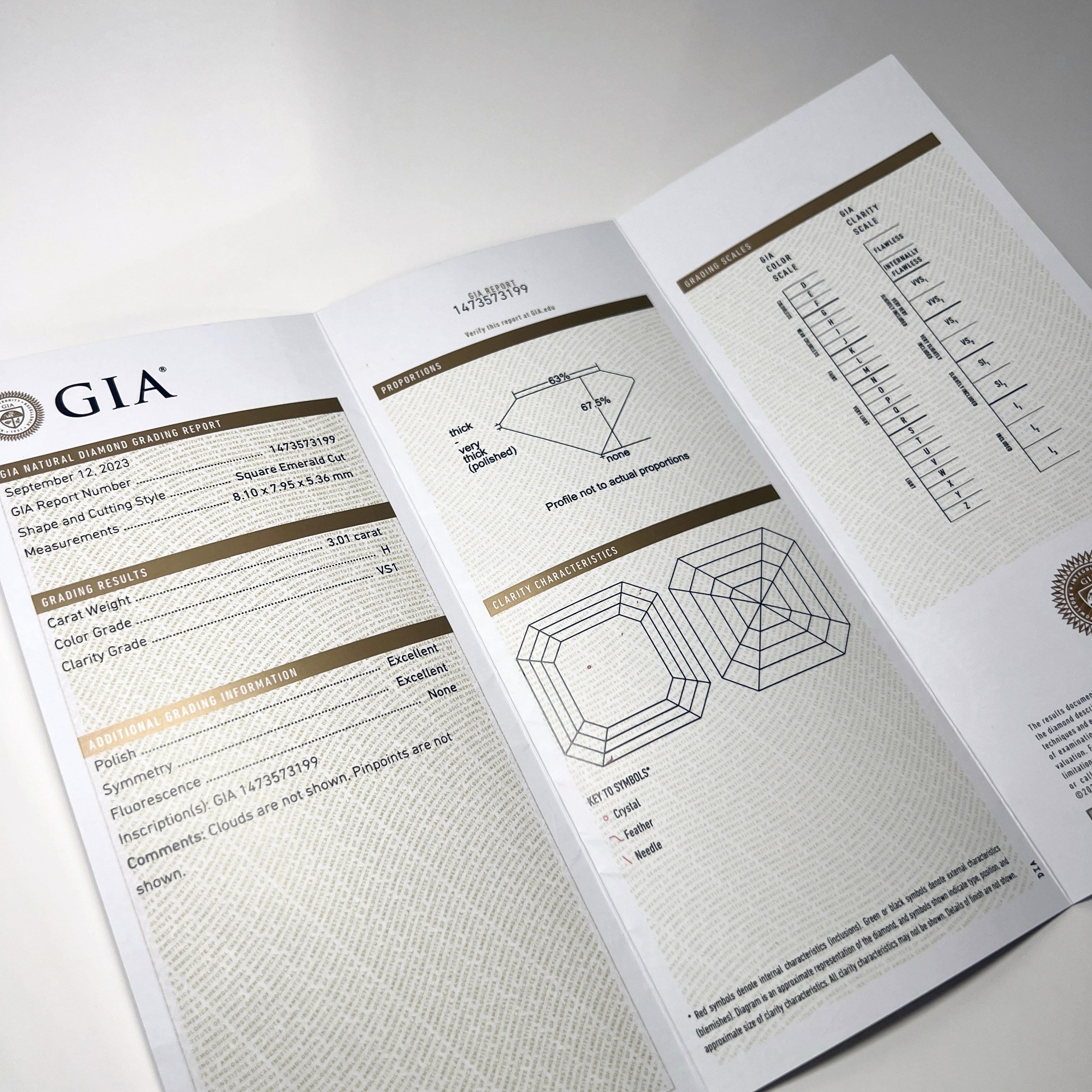

Have your diamond ring appraised professionally to help determine its value. Regularly update the appraisal every 2 years, as natural diamonds tend to appreciate in value. It’s also important to note that a diamond grading report you may receive with your engagement ring is not an appraisal.

Opt for jewelry insurance that covers loss, theft, and damage. Consider a scheduled jewelry policy for comprehensive protection.

Maintain detailed records, including photos, receipts, and appraisals to support any future jewelry claims.

Ensure your policy reflects any changes in your ring’s value, particularly after resizing, setting modifications, or market fluctuations.

When not wearing your ring, store it in a secure location. Avoid keeping multiple valuable items in the same place to reduce the risk of losing everything in a single incident.

Have your engagement ring inspected at least once a year. Regular inspections help ensure that the diamond or gemstones are securely set, and that the band and prongs haven’t succumbed to wear and tear. Some insurance providers may even require annual inspections to keep your jewelry insurance valid.

Travel with confidence and enjoy your engagement ring, while taking practical steps to protect it, like using a hotel safe when it’s not being worn. Many couples choose providers like Jewelers Mutual for streamlined digital quotes and jewelry-specific policies.

Jewelers Mutual Engagement Ring Insurance backed by 12,000+ 5-Star Reviews

While your homeowners or renters insurance policy may provide some coverage for jewelry, it’s often limited—and not nearly enough to protect your engagement ring. Jewelry is typically categorized under personal property, meaning it’s covered in the event of a catastrophic loss, such as a fire. However, that coverage may be shared with all of your belongings. For example, if your policy includes $100,000 in personal property coverage, that amount must cover everything from clothing and furniture to electronics and décor—your jewelry included.

Even more concerning, standard policies come with strict limits. Most only cover jewelry theft up to $1,500, regardless of how much personal property coverage you have. Worse, they typically do not cover accidental loss, disappearance, or everyday damage—some of the most common risks engagement rings face.

Additionally, filing a jewelry claim can increase your homeowners insurance premium, and any payout will likely have a deductible subtracted. For those with a high-value ring, relying on a standard policy could leave you significantly underinsured. That’s why many couples opt for additional jewelry-specific coverage for their protection.

With dedicated jewelry insurance, claims generally won’t impact your homeowners coverage, helping protect both your jewelry and your home insurance policy.

Standard homeowners or renters insurance policies may include limited jewelry coverage, but coverage caps are often low and certain causes of loss may be excluded. In many cases, the coverage available may not be enough to fully replace a valuable engagement ring.

Adding a rider can increase coverage for specific items, but terms, limits, and covered events vary by policy and carrier.

A personal property floater can provide additional coverage for a specific item, such as an engagement ring, and may offer protection against certain types of loss or theft. You’ll typically need an appraisal for each item. However, coverage varies by insurer and policy, and some floaters may not cover damage, mysterious disappearance, or other types of loss.

While these options can increase protection, they still may have limitations compared to a dedicated jewelry insurance policy. In addition, filing a jewelry claim through your homeowners insurance could result in higher premiums or, in some cases, affect the renewal of your policy. Dedicated jewelry insurance is designed specifically for valuable jewelry and often provides broader coverage and specialized protection.

For the most comprehensive protection, a standalone jewelry insurance policy is the best option for ring insurance.

Companies like Jewelers Mutual specialize in protecting engagement rings with policies tailored to fine jewelry. Unlike standard homeowners or renters insurance, these policies are designed to cover loss, theft, accidental damage, and disappearance.

One of the biggest perks of specialty jewelry insurance is the added benefits. Many policies cover preventative maintenance—such as prong tightening, repairs, or even replacing a lost stone—helping to keep your ring in its best condition. Plus, instead of providing a payout, these insurers often work directly with your jeweler to replace or repair your ring, helping to provide a comparable piece based on your policy terms without the hassle.

Another major advantage? Filing a jewelry claim won’t impact your home insurance policy or cause your premium to rise. This makes standalone jewelry insurance a smart decision for anyone looking to protect both their ring and their overall financial security.

Absolutely! Vintage and antique engagement rings can (and should) be insured, but they often require a bit more attention when choosing the right policy. Because these rings are one-of-a-kind and may have unique craftsmanship or rare gemstones, insuring them properly ensures they can be repaired or insured to the full documented value.

The first step in insuring a vintage or antique ring is getting a professional appraisal from a jeweler who specializes in antique pieces. This appraisal should detail not only the ring’s market value but also its historical significance, craftsmanship, and any unique features.

When choosing a policy, look for coverage that includes antique and estate jewelry to ensure your ring is protected. Specialty jewelry insurers often have policies designed for vintage pieces, offering options for repair or replacement that honor the ring’s originality. Since antique rings can be difficult to replace exactly, some policies allow you to work with a jeweler to create a custom reproduction if necessary.

The cost of insuring your engagement ring is surprisingly affordable. On average, jewelry insurance costs between 1–2% of your ring’s value per year. That means insuring a $5,000 ring would typically cost between $60 and $100 annually—a small price to pay for peace of mind.

Several factors can influence your ring insurance premium, including your location, the ring’s value, and the type of coverage you choose. Some insurance providers also offer discounts if you have a home security system, a safe, or other protective measures in place. Ultimately, jewelry insurance is an easy and cost-effective way to protect your most treasured piece.

Providers like Jewelers Mutual offer flexible pricing and quick online quotes, making it easy to protect your ring in minutes.

Insuring your natural diamond engagement ring helps protect not only the value of your ring but also its emotional value. With the right coverage, you can wear your heirloom worry-free, knowing it’s safeguarded for the future.

Your engagement ring represents a moment you’ll never want to lose. With the right insurance, you don’t have to.

Jewelers Mutual Engagement Ring Insurance backed by 12,000+ 5-Star Reviews

Although Natural Diamond Council may offer opinions to consumers about the importance of protecting their purchases, Natural Diamond Council is not a licensed agent and does not sell or offer advice about insurance. Any/all decisions for protecting jewelry must be made by the consumer, following information gathering. The purchase of insurance must be done by direct interaction with an insurer or licensed insurance agent.

Coverage is offered by either Jewelers Mutual Insurance Company, SI (a stock insurer) or JM Specialty Insurance Company. Policyholders of both insurers are members of Jewelers Mutual Holding Company. Any coverage is subject to acceptance by the insurer and to policy terms and conditions.

By clicking the link above — “get a quote” — you authorize Jewelers Mutual to use a secure system to retrieve and save details of this purchase from us for the purpose of calculating an insurance quote. Retrieved information may include your name and address.

The information above provides general descriptions of coverage that may or may not apply to your policy. Coverage options may vary by state and product, and some exclusions or limitations may apply. Please review your policy contract for specific details.